|

Capital in Netherlands

1921-2013 & Piketty’s formula

Summary

Summary of

article in ESB Jaargang 100 (4704) 26 February 2015,

by Dr. Marein van Schaaijk

Click

here to download Kapitaal NLD.xls with the

underlying data

FORMULA

Piketty

(2014) presents in his splendid book for several countries for several

periods

a treasury of data concerning the private rate of return on capital, r,

the

rate of growth of income and output, g and the capital/income ratio,

K/Y. Based

on his empirical analysis using graphs, he finds his third formula: The

Central

Contradiction of Capitalism: r > g. His conclusion is:

“The principal destabilizing force

has to do with the fact that the private rate of return on capital, r,

can

be significantly higher for long periods of time

than the rate of growth

of income and output, g. The inequality r

> g implies

that wealth accumulated in the past grows more rapidly than output and

wages.”

However, ”significantly higher for

long periods of time” what

does that

exactly mean? So first we try to find out what is exactly the relation

between,

r, g and K/Y.

In sheet

Formulas in Van Schaaijk,

2015, you can find that there exists a definition relation:

p*r –g = z

in which p = dK/W (the investment

ratio / profit rate), and z the percentage growth rate of K/Y

Given this definition follows: If r

> g/p then z > 0

However

Piketty’s conclusion “The

inequality r > g implies

that wealth accumulated in the past

grows more rapidly than output and wages”, is only true for

certain values of

p.

So if

you change in the third

formula of Piketty ”significantly higher for long periods of

time” into

“1/p” then Piketty’s third formula

becomes a definition equation, and that is true always and everywhere.

So not

only this century but also next and not only in the countries that

Piketty

studied but all countries. So

no

empirical work needs to be done to come to this conclusion for example

for the Netherlands

during 1921 – 2013.

Actually, also concerning the

second

formula of Piketty a definition equation can be derived, see in sheet

Afleiding

formules in Kapitaal NLD.xls.

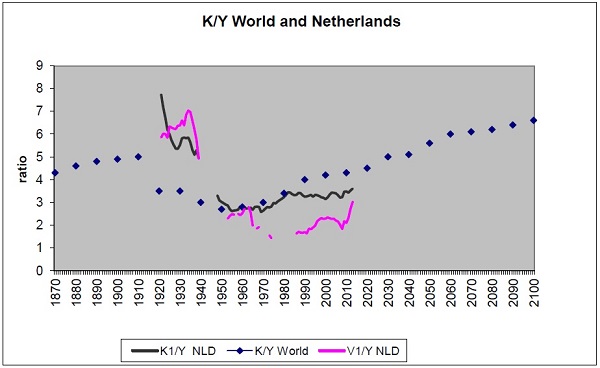

Capital

in Netherlands 1921-2013

A lot

of methodological problems are

there when calculating longer time series for capital. See Coenen, ESB,

26-2-2015. We made several time

series, see KapitaalNLD.xls

on www.micromacroconsultants.com

In the

graph below we present two of

them for the Netherlands

for the period 1921-2013. One V1/Y NLD, based on wealth statistics, and

the

other one K1/Y NLD based on cumulated net real investments with

starting point taken in 1947 from the figure of the wealth statistic.

Furthermore in the graph below

we

show the K/Y for the World 1870-2100

from Piketty’s graph 12.4

Source: Piketty, 2014 Graph

12.4 and van Schaaijk,

KapitaalNLD.wks January 2015

The

graph shows big differences

between K1/K NLD and V1/Y NLD, but in both cases there was a big

decrease

between 1921 and the seventies (in Netherlands much more then in the

World), then

a slight increase, followed by stabilisation of the last thirty years

in case of K1/Y,

but some increase in V1/Y. In the World the last thirty years show an

increase, and

Piketty expects a further increase.

Conclusions

In

this article is shown that

Piketty’s third formula could be made more precisely by

bringing in it a factor

p (the ratio of investment/profits). Then a definition equation

results. Such

equations do not need to be proved by empirical analysis. So instead of analyzing r

and g one can

immediately start analysing K/Y. That

is

what has been done for Netherlands.

Is the decrease of K/Y between 1921

and the seventies the result of capital saving technical progress or

changes in

wage costs per product? It

might be

interesting to analyse Dutch capital stock data that are available per

sector

of industry.

Answering those questions is beyond

the scope of this brief article.

Literature:

- Piketty, T., Capital

in

twenty-first century, The Belknap Press of Harvard

University Press.

Cambridge, Massachusetts, London, England,

2014

- Van Schaaijk, M. van (2015) KapitaalNLD.xls (in

Dutch) on www.micromacroconsultants.com

- Schaaijk,M. van (2015) Kapitaal in Nederland,

ESB Jaargang 100 (4704) 26 February 2015

Addendum

2nd March 2015

We mentioned already that also concerning the

second formula of Piketty a definition equation can be derived. What does this

mean?

We know:

z = k – g The percentage growth

rate of K/Y z, is the percentage growth rate of capital k, minus the percentage

growth rate of Y, g. And savings rate s

= S/Y*100.

k = dK/K *100

= (dK/S)*(S/K) *100 =

(dK/S)*(S/Y)*(Y/K) *100

so k = (dK/S)*s/(K/Y)

so z = (dK/S)*s/(K/Y) - g

so

if z = 0 and dK=S then

K/Y

= s/g This is Piketty’s second formula

Please

note that K/Y = s/g is only true if z =

0 and dK = S It is a little bit

strange to use this formula that assumes K/Y to be stable, to forecast changes

in K/Y.

Piketty

assumes that world g will decrease from more then 3 now to below 1,5 and that s

will stabilise around 10 percent. If in the formula K/Y = s/g you divide g by 2, then K/Y will become twice

as big. And that is what Piketty shows in his graph 5.8. His main conclusion

and fear is that K/Y will increase a lot this century, and might even go up to

the level of the beginning of last century.

However

assume for example g becomes 0, then, following Piketty’s formula, K/Y becomes

infinitive (!?) and should g change from 3 to – 3 then K/Y does not change in

number, but becomes negative (!?)

So

it looks like that Piketty’s second formula cannot be used to forecast K/Y.

Piketty

wrote a beautiful book with a lot of interesting information, only he might

reconsider to revise his second and third formula. That could also result in

another conclusion concerning K/Y growth during this century.

He

might just use z = k – g if he wants to

forecast the effect of X lower increase in g (because of lower population

growth) on z. All other things equal (like k)

X lower g means X higher z.

But K and g are not independent of each other.

If g goes down businesses need less growth of machinery and buildings, so

sooner or later you might expect also k to go down. In case savings at the same

time go up (because maybe expected ageing of population in the future one might

save more now). Thanks to deficits on the capital account of the Balance of

Payments, the national Wealth/ Y ratio might increase even when domestic K/Y is

stable.

|